In most broker conversations I have, the problem sounds like leads. It almost never is.

Ask a busy mortgage adviser what is holding them back and you will hear about lead volume, portal costs, or the price of a qualified enquiry. It is a reasonable answer, and in my experience the wrong one. The leads are usually there. What is broken is the gap between the enquiry landing and the appointment sitting in an adviser's diary, and that gap is pure admin: the fact-find, the protection follow-up, chasing documents, and finding a slot in a calendar nobody outside the firm can see.

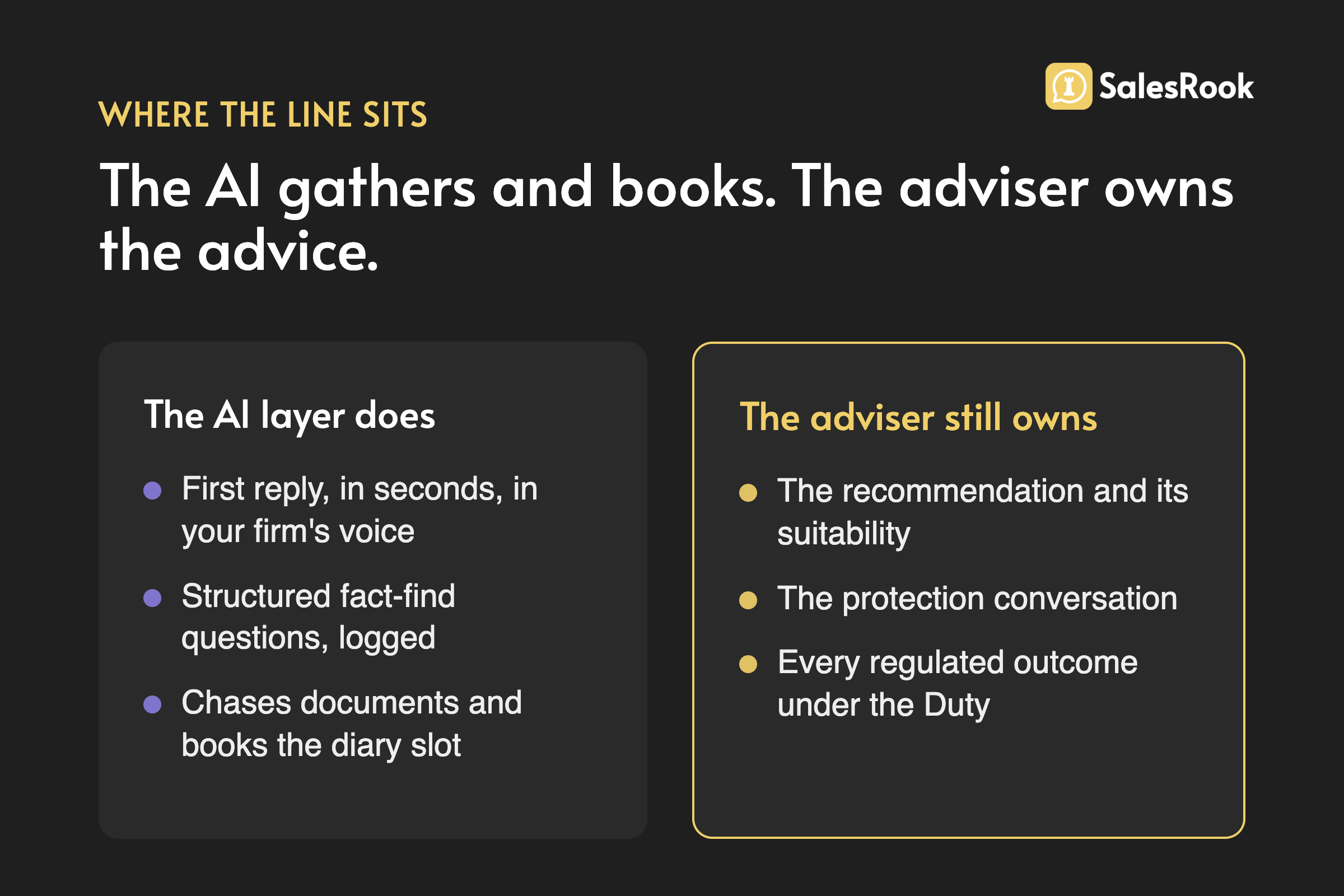

I want to make an honest case for where artificial intelligence genuinely helps with that admin, and where it has no business going. This is a regulated business, so the adviser owns the advice, full stop. But a great deal of what eats a broker's day is not advice at all. It is the drag around it, and that is the part this piece is about. The wider picture sits in our guide to mortgage broker Consumer Duty compliance; here I am staying narrowly on the admin.

The bottleneck is not leads. It is the admin between the lead and the appointment.

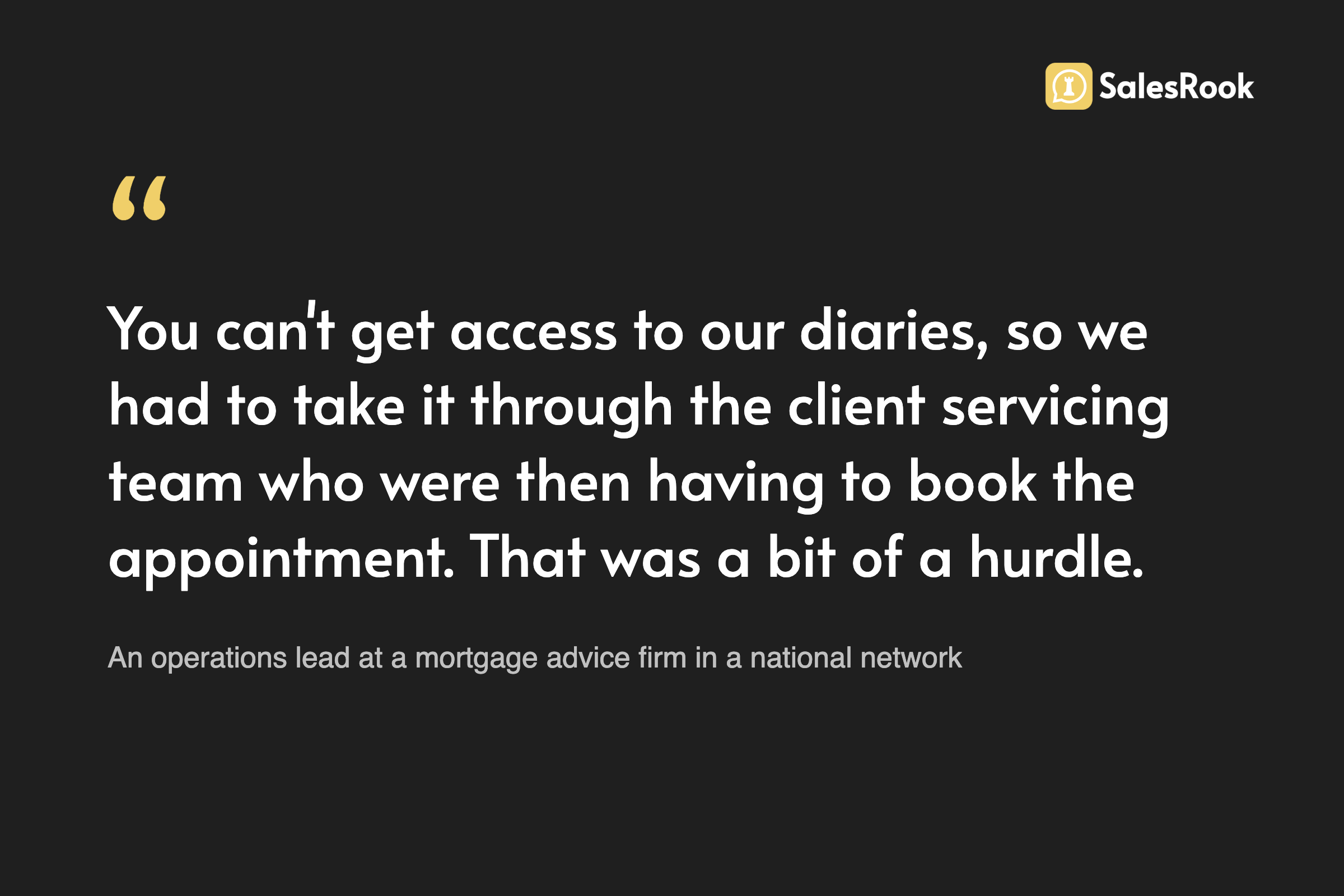

A qualified lead is worth nothing until it is inside an adviser's diary, and the diary is often the one thing a first-response process cannot reach. An operations lead at a mortgage advice firm in a national network put it to me plainly:

That is the whole problem, and notice the relay it creates. A warm enquiry comes in, someone qualifies it, and then it stalls because the person who did the qualifying cannot see when an adviser is free. So it gets passed on, re-typed, and booked by hand later, and somewhere in that relay the borrower can cool, or simply go elsewhere. Multiply that by every enquiry, and you can see why firms carry so much support headcount.

None of that admin is advice. It is the connective tissue around the advice, and it is expensive. One adviser-technology provider estimates the average adviser completes around nine mortgages a month while losing over 14 hours a week to repetitive admin, duplicated data entry and manual case handling. Treat that as directional rather than gospel, since it is a vendor's own figure, but the shape of it will feel familiar to anyone who has ever run a broker firm.

What the admin drag actually looks like

Break the drag into its parts and it is always the same four jobs, in the same order, done by hand.

- The fact-find. The first-pass gathering: name, situation, rough loan size, timescale, whether there is a partner on the mortgage now, whether there are dependants. Not the regulated advice conversation, the groundwork before it.

- The protection follow-up. The "we should also look at your life and income cover" nudge that a stretched team rarely gets round to. It matters more than ever: new protection sales fell across most lines in 2025, with life assurance new business down more than 11%, on Swiss Re's Term and Health Watch numbers.

- Chasing documents. The payslips, the ID, the bank statements. The polite third reminder nobody enjoys sending.

- Booking the diary. The bit that stalls, as we just saw, because the diary is a walled garden.

That second job is the one that dies quietest, and not because advisers do not care. While we were planning re-contact campaigns with a UK mortgage brokerage, going back to mortgage clients who had never taken the protection conversation, one of its directors described exactly how the follow-up gets lost:

"Our historic conversion rate on protection is low. You're talking 20 something percent, which is lower than where we want it to be. But the individual advisors are extremely productive, but they shoot fish in a barrel. You know, they have some opportunities coming at them that they lose stuff and just move on."

A director at a UK mortgage brokerage

Sit with what he is conceding there. His advisers are good. The follow-up still dies, because a productive adviser's day is already full of the deals directly in front of them, and the client who deferred the protection conversation quietly never gets asked again. Telling a busy team to try harder has never fixed that. The follow-up has to stop being a task somebody remembers and become a process that runs.

Now put that against the calendar. UK Finance forecasts roughly 1.8 million fixed-rate deals expiring in 2026, up from about 1.6 million the year before. Many of those borrowers need a fresh conversation, and ideally a protection review to go with it. The demand is not the problem. The problem is that a four-part manual process does not scale to meet it, and the follow-up is usually the first casualty.

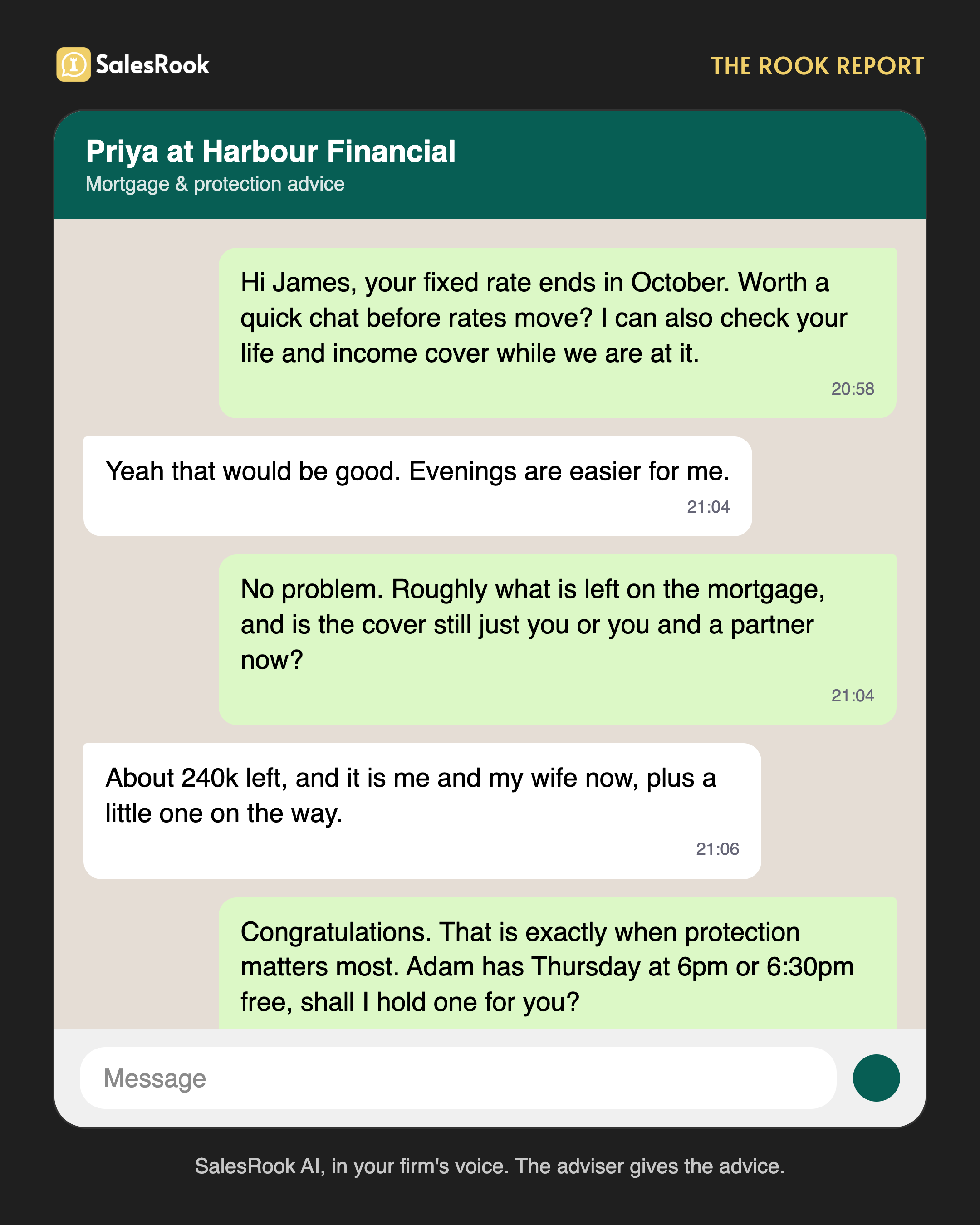

The follow-up a stretched team rarely makes, made on the channel people actually reply on. The adviser still gives the advice.

This is the same leak we wrote about on the sales side in the renewal wave and product-end-date outreach. The enquiries are not being out-marketed.

They are being out-admin'd.

The line the AI must not cross

Here is where I get cautious, and where you should be sceptical of anyone who is not. A mortgage recommendation is regulated advice. A protection recommendation is regulated advice. The suitability of both sits with a human adviser and their firm, and no amount of clever automation changes that. The FCA's 2026 mortgage priorities are blunt about it: advice must be suitable for the customer's actual needs, not just a box confirming they qualify, and record-keeping must clearly show that advice was tailored and appropriate.

The regulator is equally clear that reaching for a tool does not move the responsibility. Under Consumer Duty, the firm must put its customers' needs first and evidence good outcomes across the whole journey.

And when a firm leans on a third party or a piece of software to do part of the work, the FCA's position on outsourcing is unambiguous:

"Your firm is responsible and accountable for all the regulatory responsibilities that apply to outsourcing and third party service arrangements. Firms cannot delegate any part of this responsibility to a third party."

FCA, on outsourcing and operational resilience

That principle runs right through the Handbook's rules on outsourcing: a firm that outsources a function remains fully responsible for discharging its obligations.

Software does not sign the suitability report. The adviser does.

Consumer Duty puts the outcome, not the tooling, at the centre. The tool can help; the accountability stays with the firm.

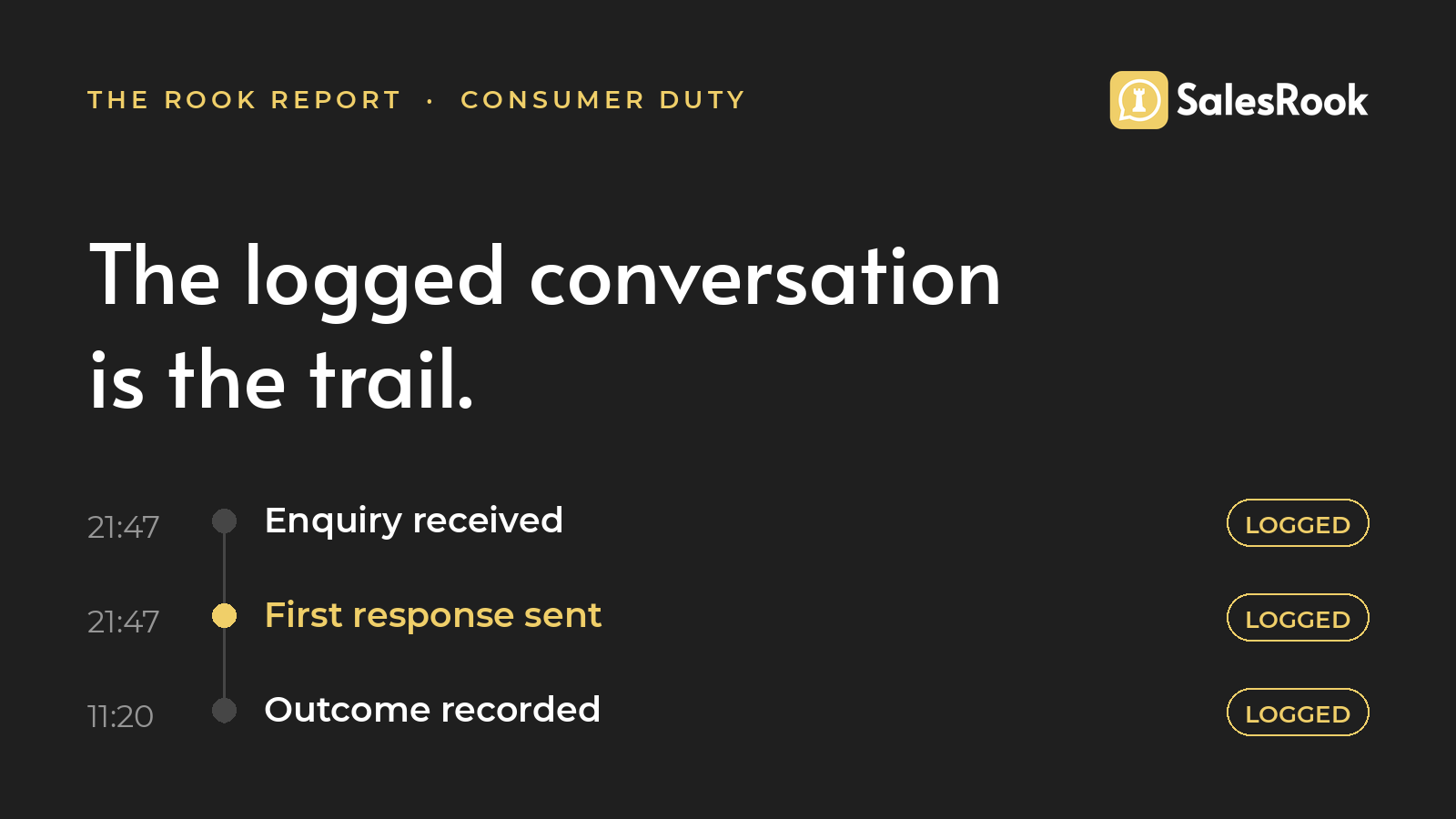

So the test for any AI in a broker's workflow is simple. Does it gather, log and book, leaving a clean audit trail for the adviser? Or does it try to advise? The first is a genuine help. The second is a compliance problem wearing a helpful costume. Encouragingly, the FCA itself has landed in roughly the same place: reviewing AI in mortgage advice at the end of 2025, it found existing frameworks already able to manage the risks, and a strong consensus that AI should improve the advice process, not replace the adviser.

Where a fast, logged first response safely helps

Stay on the right side of that line and the opportunity is real, because the admin drag is largely made of jobs that are repetitive, rules-based and auditable. Picture the layer doing exactly four things: replying in seconds in your firm's own voice; asking the structured fact-find questions and logging every answer; chasing the outstanding documents; and, crucially, reading the advisers' live calendars and booking the borrower straight into a real slot.

That last point is what dissolves the diary hurdle from the top of this piece. Instead of passing a lead to a servicing team to book by hand, the layer checks the advisers' calendars, applies whatever rule the firm wants (round robin, preference, or simple availability) and books directly, then writes a note to the file so the adviser walks into the appointment already briefed.

The hurdle was never the borrower's willingness. It was the handoff.

The document chase deserves the same precision, because it is easy to automate the wrong thing. On one of our own build calls I described document collection as a bit of a faff, a friction point to be smoothed away, and the broker we were building for corrected me on the spot:

"You say it's a friction point, but it's a friction point that the client's going to need to act on it. They're going to need that at some point. I would rather have it up front so that I can identify exactly what they're telling me. You know, some client might tell you, Max, they're earning £50,000 when they're not actually earning £50,000 or they've got a big card payment coming off through salary sacrifice. You know, so these are the wee things that they might not tell you that's absolutely evident in the documents that are there."

The principal of an independent mortgage brokerage, on a SalesRook build call

He is right, and being corrected by your own customer is a fast way to learn what your product is actually for. The ask is not the drag. The ask is the fact-find doing its job, surfacing on paper what a borrower forgets, rounds up or would rather not mention. The drag is a stretched human spending the week sending the polite third reminder. So the layer does not make the documents optional; it makes the chasing prompt, consistent and logged, so the papers arrive before the appointment does.

Speed matters here more than brokers sometimes admit. When Street Group surveyed 1,830 sellers in July 2026, 85% said they expect a reply within 24 hours, and more than 63% expect the same working day. That is seller-side evidence, not a mortgage-borrower figure, but it is a fair read on how fast people now expect anyone to reply. A first response that arrives in seconds, on WhatsApp, where our own conversations see reply rates approaching 87% against roughly 20% for email, is not a gimmick. It can be the difference between a booked appointment and a cold lead.

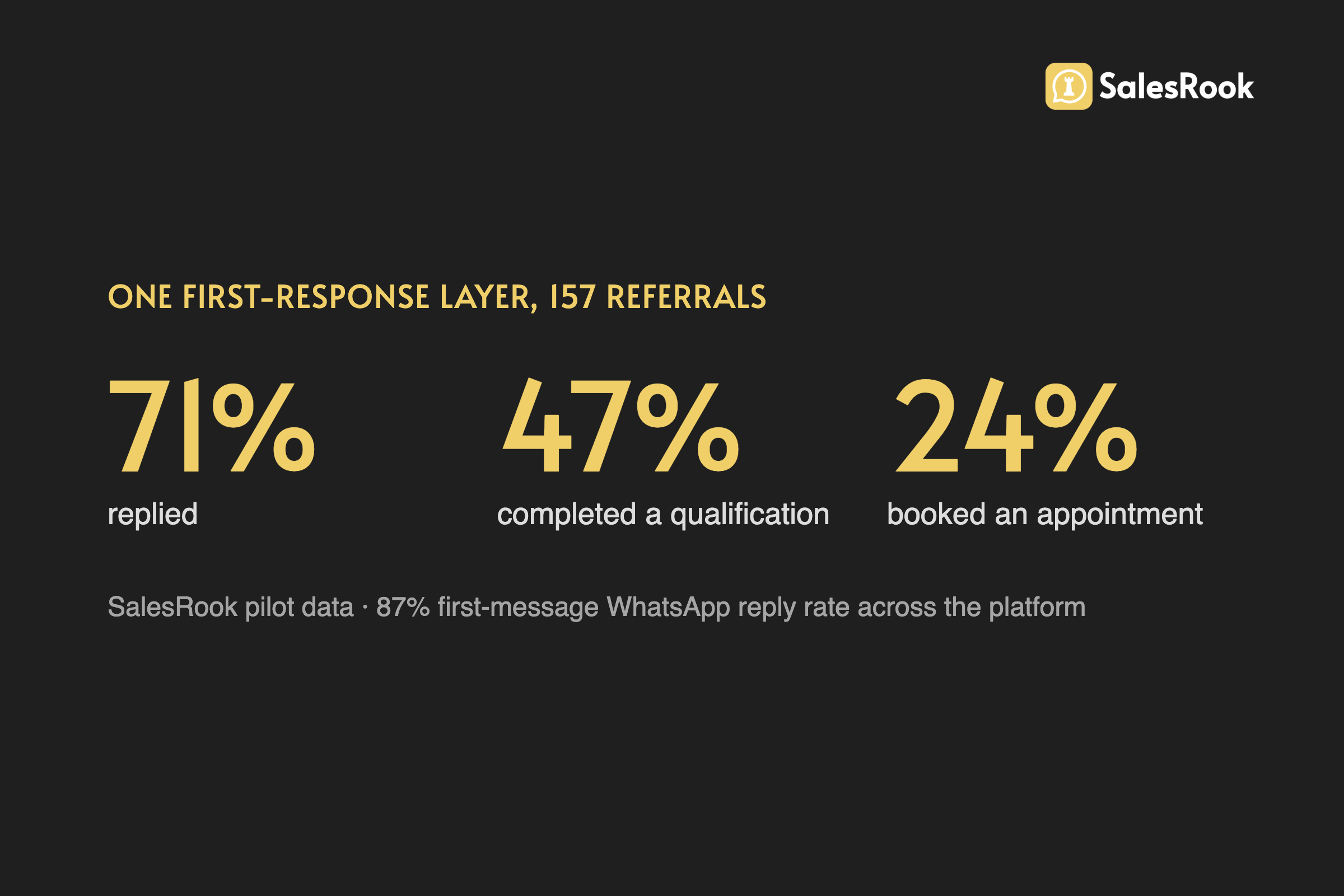

When we run that layer across real referrals, the shape is consistent. Across 157 handed-off mortgage referrals, 71% replied, 47% completed a qualification, and 24% went on to book an appointment. Reaching back out to existing customers whose product is ending, a single well-timed message books a meeting with around 31% of them. These are our own platform figures, not an independent audit, so weigh them as such. But the pattern is not subtle.

The numbers from a real broker pilot

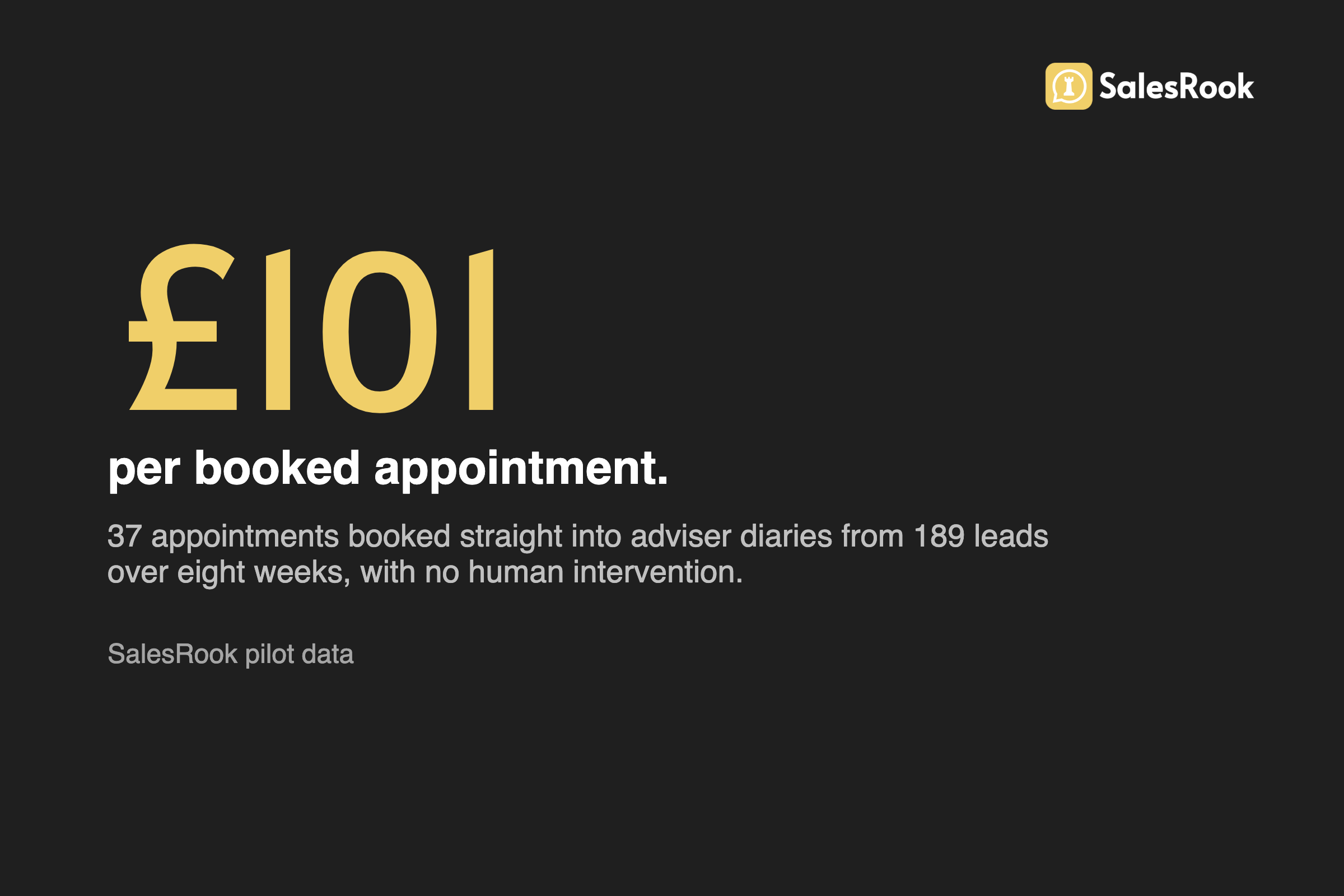

The figure I keep coming back to is cost per booked appointment, because it is the one that maps cleanly onto a broker's economics. In an eight-week pilot with a partner advisory firm, spread across seven introducing agencies, the layer handled 189 leads. Around three quarters engaged, half qualified fully, and 37 booked straight into adviser diaries with no human intervention at all.

£101 per booked appointment

37 appointments booked into adviser diaries from 189 leads over eight weeks, with no human intervention. Set against paid mortgage leads that can run £30 to £70 before any qualification at all. SalesRook pilot data.

A booked appointment for a bit over a hundred pounds is a different unit of value from a raw lead for thirty. And here is the honest footnote, which cuts both ways: that pilot ran completely unoptimised, with no human follow-up on the warm-but-unbooked leads, for want of resource. We do not actually know what those leads would have converted at with proper human chasing, because that test was never run. Our own reading is that results should improve for the same spend once a lead qualifier works the ones who shared their numbers but did not book, but that is a projection, not a result.

Either way, the drag you remove is not a rounding error. It is measured in adviser hours, and in the appointments that used to die in the handoff.

Keeping the human adviser central

If any of this reads as "the machine replaces your advisers," I have written it badly. The whole point is the opposite. Take the admin off an adviser and you do not get a smaller adviser, you get a busier, better-used one, spending the day on the regulated conversation they are actually paid for rather than on chasing a payslip. The protection gap does not close by sending more reminders by hand; it closes when the follow-up happens reliably and the adviser is free to have the real conversation when the borrower turns up already qualified.

The admin the AI absorbs is the fact-find scaffolding and the chasing. What the freed hours buy back is the protection conversation, the regulated part a borrower is actually paying an adviser for.

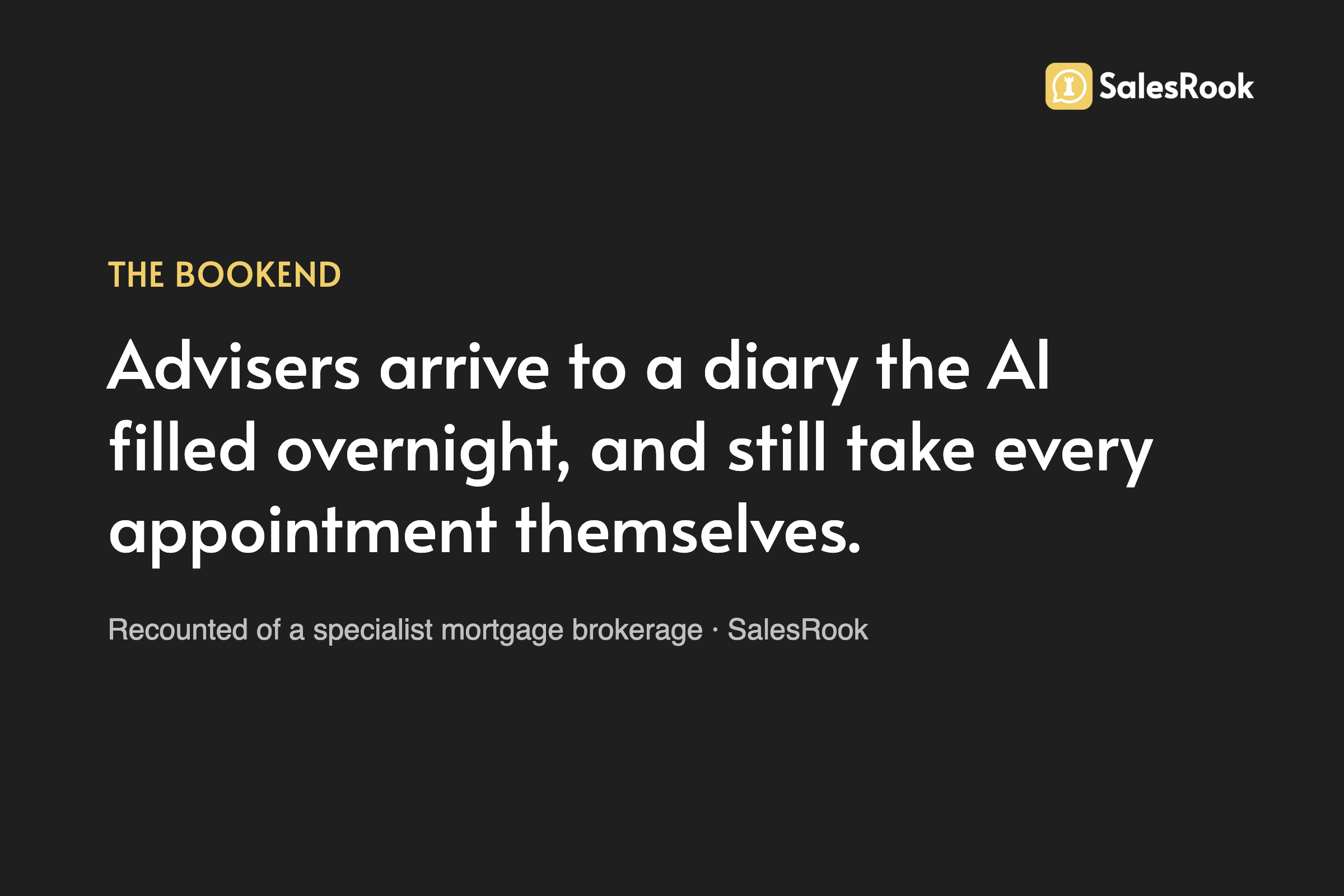

There is a moment that captures it. SalesRook describes a specialist brokerage where the advisers arrive in the morning to find appointments already sitting in their calendars, booked by the AI at ten o'clock the night before.

The diary nobody outside the firm could see is now a diary that fills itself overnight, and the adviser still takes every appointment and owns every recommendation. That is the shape of AI that helps a broker: it does the drudgery, it keeps the receipts, and it hands the human a warm, briefed borrower at a sensible time. Much of this help comes from the enquiries that originate with estate-agent partners in the first place, which is a whole discipline of its own; if that is your channel, our estate-agent lead generation work is the companion piece.

What to measure on Monday

You do not need to buy anything to find out whether admin is your bottleneck. You need to count it. So here is the one thing I would do this week, before you weigh up any protection admin software or fact-find automation at all.

Open last month in your CRM. Take every enquiry that came in, and sort them into three piles: the ones that got a first reply within the hour, the ones where a fact-find was actually completed, and the ones that ended in a booked appointment without a human re-typing anything. Then look at how much smaller each pile is than the one before it. The drop between "enquired" and "replied within the hour" is your speed leak. The drop between "replied" and "booked" is your admin leak. That second number, in appointments you never sat, is the size of the prize, and it is often bigger than the lead-volume problem you thought you had.

Count those three piles honestly. They are your numbers, and no vendor can argue with them, including us. Then bring them to a short call, and we will walk your own month through the logged, book-into-diary layer, showing you where it would have changed the outcome and, just as usefully, where it would not.

Max Hardy

Co-Founder

Max Hardy is the Co-Founder of SalesRook, a leading provider of AI solutions for the property sector. With a background in technology and property, Max leads SalesRook's mission to transform how estate agents and mortgage brokers engage with leads through AI-powered WhatsApp automation.