In April 2026 the Financial Conduct Authority published its observations on the first Consumer Duty board reports, and the message to regulated firms was blunt. Good intentions are not the test. Firms must report every year on what their monitoring actually found about customer outcomes, and push their analysis beyond management-information dashboards to genuine insight. The bar is no longer whether you meant well. It is whether you can show it. This year, and every year after.

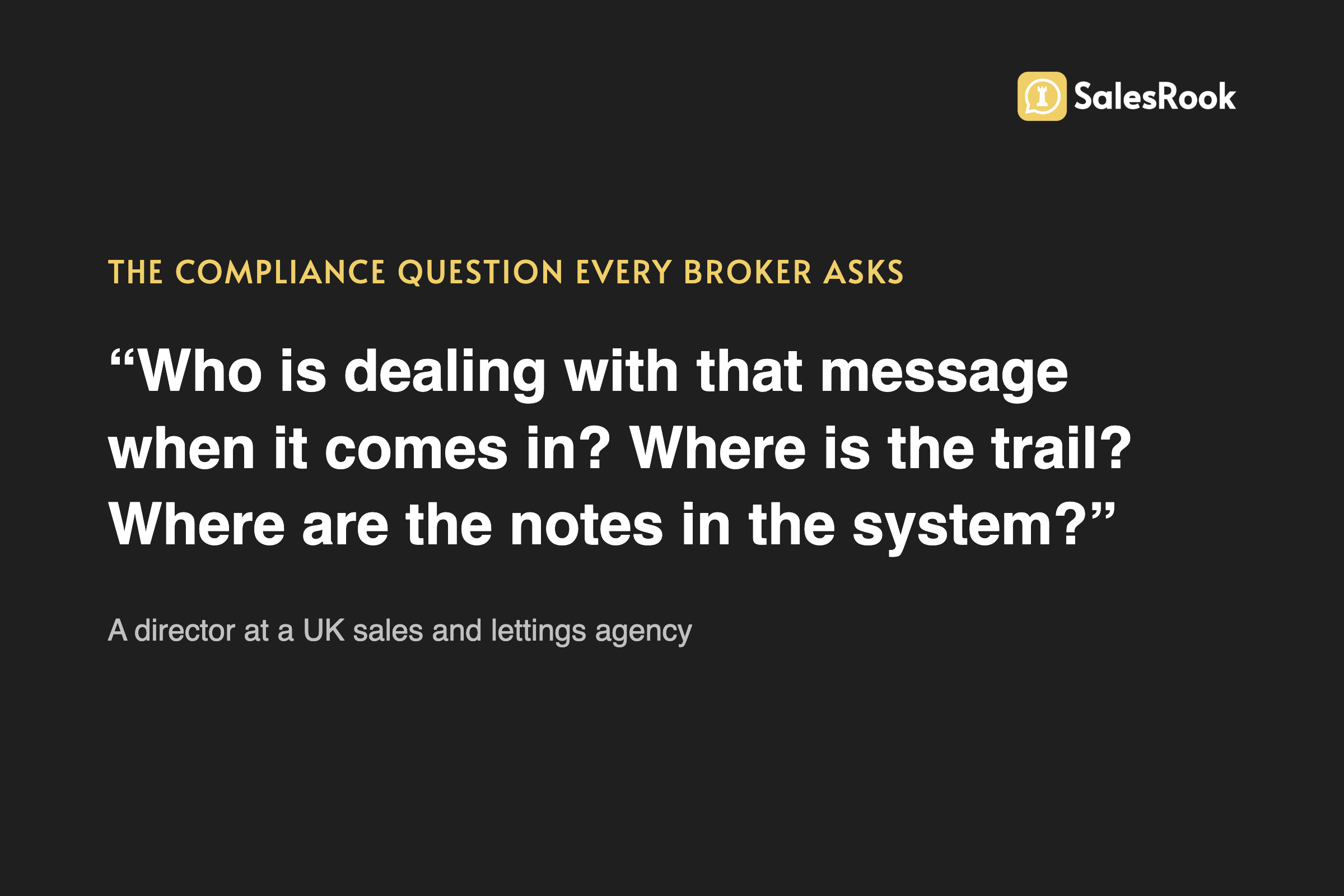

For a mortgage broker, that turns compliance from a filing exercise into an evidence problem. You already give good advice. The hard part, the part the Duty keeps pressing on, is proving it: showing that you reached the client in time, asked the right questions, and can produce the trail if anyone asks. And that is exactly the part most brokers are doing by hand, late at night, in the cracks between appointments. One man, weighing up with our team how his firm handled client messages, put the whole anxiety into a single unhappy breath.

"Who's dealing with that message when the message comes in, who's acting it, where's the trail, where's the notes in the system?"

The person who runs a UK sales and lettings agency

That is the record-keeping worry the Consumer Duty is built around, put in a real person's voice, long before anyone reaches for the regulation. He runs a sales and lettings agency rather than a brokerage, and I am not going to pretend otherwise, but the question travels: any regulated firm has to be able to answer it, and a broker has to answer it to the FCA. This piece is about answering those questions, and about where a fast, logged, consistent first response genuinely helps you meet your obligations rather than quietly adding to them. One thing up front, and I will keep returning to it: nothing here makes you compliant. You are the regulated firm. The most any tool can do is help you evidence the good outcome and reach the client in time.

What the Consumer Duty actually asks of a mortgage broker

The Consumer Duty came into force on 31 July 2023, and it applies right along the mortgage distribution chain, brokers and intermediaries included. It sits on top of one deceptively simple principle. In the FCA's own words, a firm must act to deliver good outcomes for retail customers. Underneath that sit three cross-cutting rules, act in good faith, avoid causing foreseeable harm, and enable and support customers to pursue their financial objectives, and four outcomes covering products and services, price and value, consumer understanding, and consumer support.

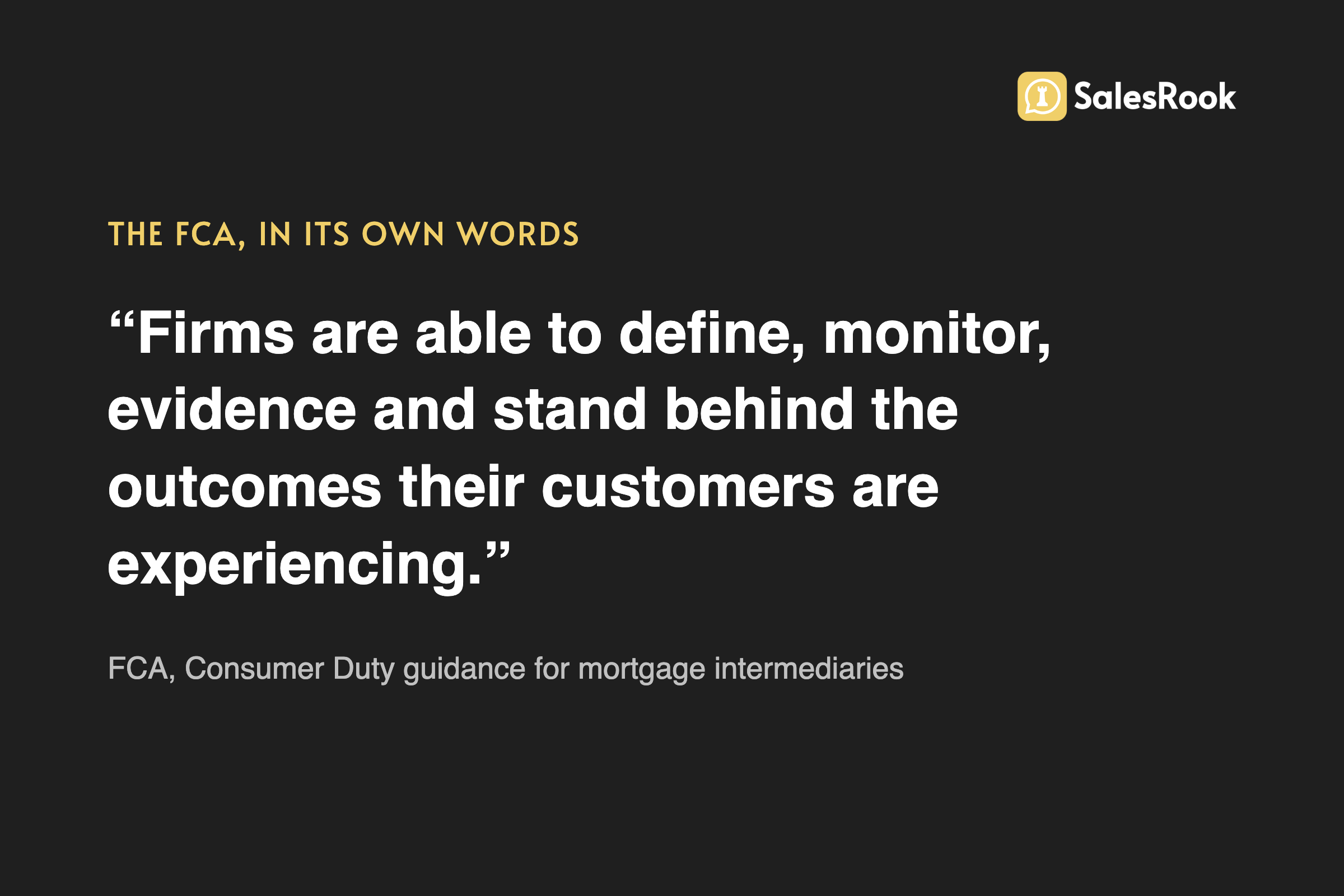

None of that will surprise a good broker, because a good broker already does it. The shift the Duty introduced is not the standard of advice. It is the burden of proof. As the FCA told mortgage intermediaries directly, a key part of the Duty is that firms are able to define, monitor, evidence and stand behind the outcomes their customers are experiencing. Read that sentence slowly.

It is not asking you to be a better adviser. It is asking you to be able to prove you were one.

It helps to translate each outcome out of regulator-speak and into the things that happen in your day. Here is my plain-English read of how the four outcomes land on a broker's desk, and, crucially, the kind of evidence each one quietly asks for. The middle and right columns are a broker's-eye translation, not the FCA's exact words.

| The Duty outcome | What it means for a broker | What you need to be able to show |

|---|---|---|

| Products and services | The advice fits the client's needs and circumstances, including anyone with characteristics of vulnerability. | A complete, consistent fact-find, taken every time, not just when the day is quiet. |

| Price and value | The client is not left on a worse deal by default, and fees are fair for the service given. | Proof you reached them in time to act, especially at renewal. |

| Consumer understanding | The client understands their options and can make a timely, informed decision. | A record of what was explained, and when. |

| Consumer support | The client can reach you, and gets a response, without friction or delay. | A timestamped trail of the first response and every message after it. |

Look down that right-hand column. Every single one is a record. Not better feelings, not more effort, a record.

The Duty did not ask you to care more. It asked you to be able to show the caring.

And a record is precisely the thing a busy brokerage is worst at producing by hand.

The Duty is not the admin. The admin is the symptom.

Here is the honest tension at the centre of every broker's week, and it is costing you more than evenings. You came into this to advise people, to sit across a table like the one in the photo above and get a nervous first-time buyer or a worried remortgager to a good decision. What actually fills your day is the scaffolding around that: the fact-find typed into the CRM, the renewal chase, the follow-up nobody got to. At one firm I looked at, advisers were manually calling every fresh lead and doing the full fact-find by hand on the system before any advice could even begin. The regulated heart of the job had become a data-entry job.

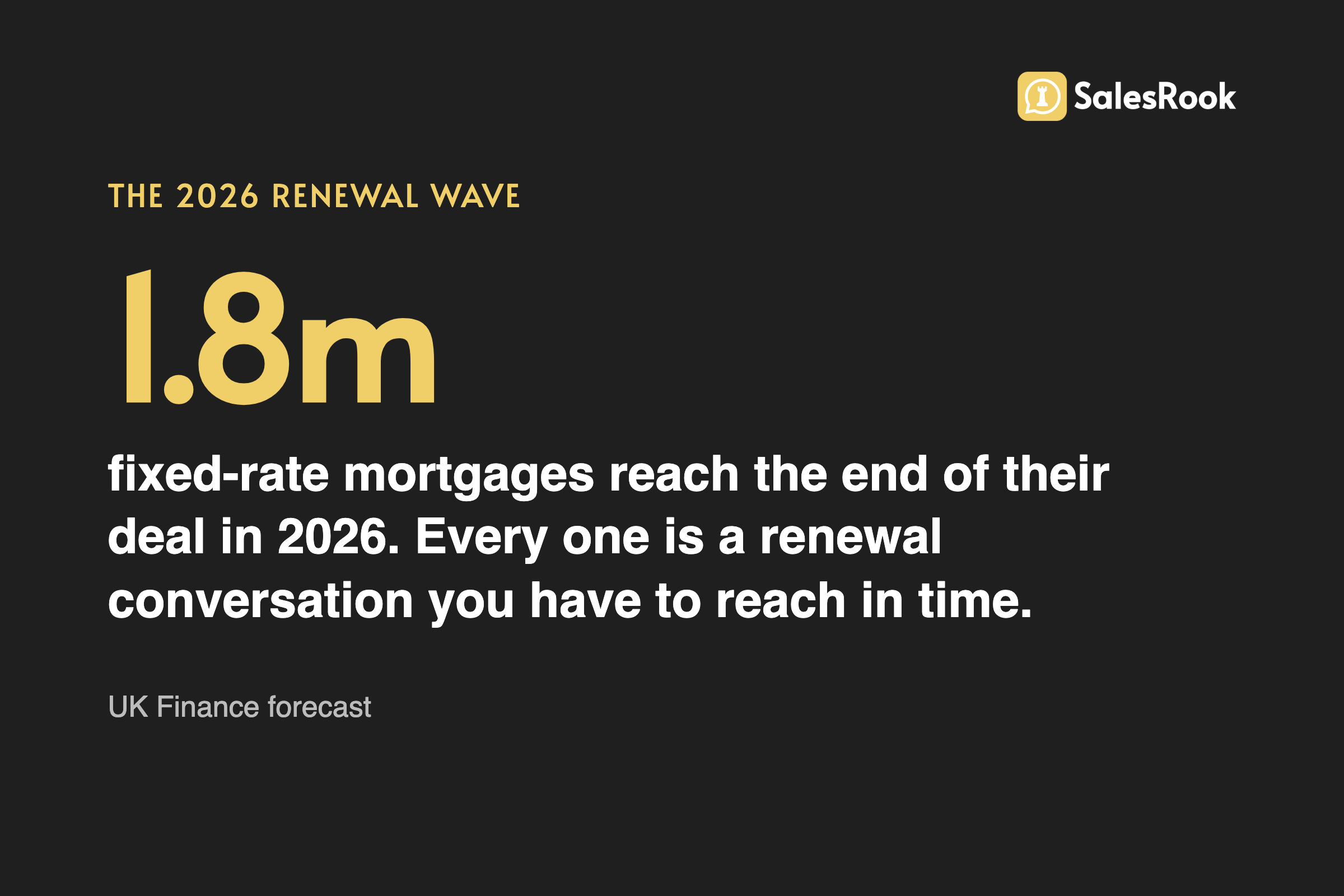

Renewals are where this bites hardest, and where the money leaks. UK Finance expects around 1.8 million fixed-rate mortgages to reach the end of their deal in 2026. Every one of those is a price-and-value moment: reach the client in time and you protect them from rolling onto a worse rate, miss them and they drift. The brokers I speak to describe a cruel window. The lender contacts the client at roughly six months out, but the broker cannot really act until around four months, and in the dead zone between the two the client is being courted by their bank while the person who actually knows their situation is not even in the conversation. Manual outreach, the calls and the mailshots, mostly misses. If you want the full anatomy of that window, we wrote about reaching the renewal wave in time separately.

Protection is the same story with a sharper edge. One mortgage and protection firm I looked at was losing hundreds of policies a month to lapses and cancellations, with almost no outreach to save them, cover the client had been advised into, quietly falling away. That is a good-outcome failure hiding in plain sight, and it is the subject of a companion piece on fact-find and protection admin that goes deeper than I will here.

The pattern across all of it is the same. The Duty is not the admin. The admin is the symptom of trying to deliver, and evidence, good outcomes with a phone, a spreadsheet and a team that is already flat out. The leads themselves are not usually the problem either; brokers are fed a steady diet of them, often from the estate agents who generate them in the first place. The problem is what happens in the hours after a lead lands, and whether any of it leaves a trail.

Where the trail goes missing

Now back to those questions. The honest answer to "where's the trail" is rarely that there isn't one. It is that there are two, and neither is the whole story. Our own sales team hears the first half in firm after firm, and I will offer it as a sales observation rather than a finding: a great deal of client contact runs over personal WhatsApp and text, on handsets the firm cannot see, log or supervise. The second half is stranger, and I only really understood it when a broker described his own setup to me.

He runs a fourteen-adviser firm as an appointed representative of a national network. The network's platform is where the regulated record lives, and he was completely candid about what he puts in it.

"All their fact finds, everything goes in there. But I only put information in to get paid. Don't chase anyone in there. Don't record anything in it other than client calls or a compliance thing."

The person who runs a 14-adviser mortgage brokerage, an appointed representative of a national network

Read that again, because it is not a confession. He is doing nothing wrong: the fact-finds are filed, the client calls are recorded, the compliance items are in there. What he is describing is a record kept for the auditor and nobody else, sitting at one remove from where the client work actually happens, which in his case is a second system he pays for himself.

He is not hiding a trail. He is maintaining one he never reads.

That is the record-keeping outcome straining before anyone has done anything wrong on the advice itself. The conversation that decides whether a client understood their options, the conversation that proves you responded in time, is happening somewhere other than the file you would hand the regulator. When the FCA asks you to stand behind the outcome, a trail you have to reassemble from two systems and a phone is a weak place to start, and "it was on Dave's phone, and Dave has left" is not an answer at all.

This is the specific place where the right tooling earns its keep, and it is worth being precise about how. If the first response goes out on a business channel the firm controls, and every message is written and stored against the client record, then the trail is not something you reconstruct later under pressure. It is a by-product of the conversation happening at all. The evidence writes itself, because the record is the conversation.

A logged conversation is the trail

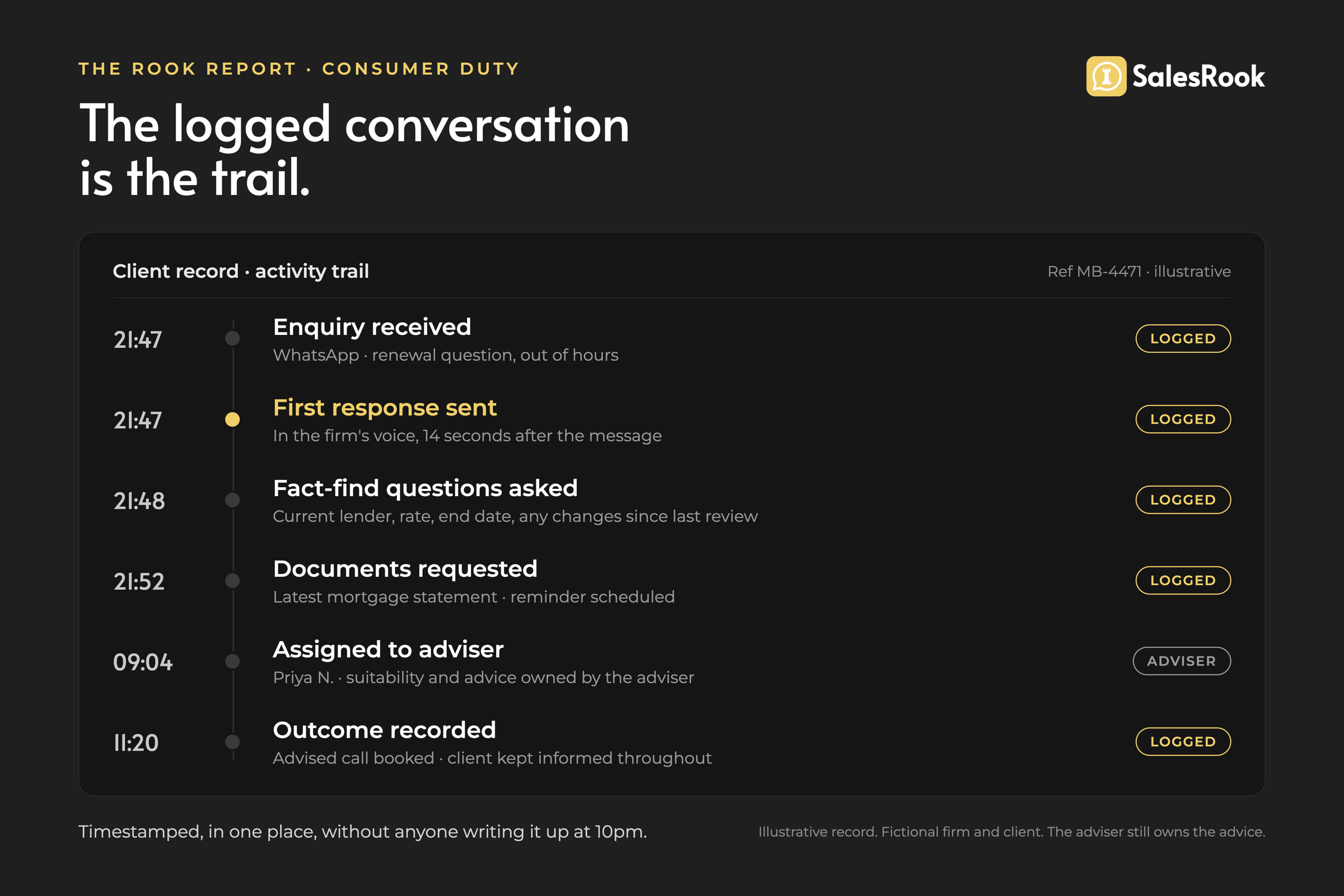

This is what we do at SalesRook, so treat what follows as informed, not neutral, and hold it to the standard in the table above. When an enquiry arrives, an AI assistant in your firm's own voice opens the conversation on WhatsApp, asks the qualifying questions a human would ask, and books the client in for your adviser. Every message is written in context rather than fired from a template, and every one is logged against the contact, with a structured outcome record handed to the adviser at the end. The point for a compliance-minded broker is not the speed. It is that the whole exchange is captured, in one place, as it happens.

A renewal enquiry, answered and logged at 00:18, in the firm's own voice. The AI qualifies and records. The adviser gives the advice.

Two things about that matter for the Duty specifically. First, consistency. A human adviser, at the end of a long week, forgets to ask a question. The system does not. It works through the agreed questions the same way each time, so the fact-find behind your products-and-services work looks the same whether the enquiry lands at 10am or, as they so often do, at 10pm, ready for the adviser to review. Second, the record. Each conversation produces exactly the trail those opening questions went looking for, tied to the client, ready to show. That is not a compliance feature bolted on. It is what a written, logged, business-channel conversation simply is.

I want to be careful here, because this is where vendors overreach. The AI does not make a suitability decision, and it does not make you compliant. It qualifies and it records. The judgement, the advice, the responsibility for the outcome, all of that stays with your regulated adviser, exactly as the Duty intends. What changes is that the adviser walks into the conversation with a complete, timestamped picture instead of a cold lead and a vague memory.

Answering in time is a Consumer Duty outcome, not a nicety

The consumer-support outcome is the one brokers most often read as soft. It is not. The FCA's own explainer on what that outcome means is worth ten minutes before your next team meeting, because it frames support as a duty, not a courtesy.

The FCA's own explainer on the consumer support outcome. Support is an obligation, not a nicety.

The market has already moved to the same place the regulator has. A Street Group survey of 1,830 home sellers found 85% expect a reply within 24 hours. That is a property-seller figure, not a mortgage one, but the expectation does not stop at the estate agent's door. Your client, mid-remortgage and anxious about the jump in their payments, increasingly expects the same of you. Answering fast, and being able to show you did, is now a real part of the evidence behind the price-and-value and consumer-support outcomes.

The gap between the enquiry and the answer is where the evidence quietly goes. I watched this land on a brokerage that was reviewing how its advisers handled a stream of referrals from an estate-agency partner. The leads were arriving. That was not the problem.

"They're coming across in the evening, brokers try and phone in the morning, and a lot of them aren't making contact."

The person who runs a mortgage brokerage, on its estate-agency referrals

Nobody in that firm is doing anything wrong. The enquiry arrives at nine in the evening. The adviser is at home, as he should be. The call goes out at nine the next morning. The client is at work. Repeat that a few hundred times and your consumer-support record is made largely of missed calls, which is a hard thing to stand behind. One of his advisers recognised the shape of it instantly, from the hardest school there is.

"You had to hit them instantly... The minute you get them, you've got to be on the phone... the heat of that lead diminishes by the minute."

A mortgage adviser, recalling the years he spent buying web leads

He learned that long before anyone was selling him AI, and the physics have not changed. What has changed is that answering at the moment of the enquiry no longer requires a human to be awake for it.

Here is one from our own records, and I am giving it to you as our data rather than a client's testimonial. A mortgage referral reached a small Scottish brokerage at a quarter past midnight. The AI opened a WhatsApp conversation in the firm's name there and then, and the client answered: what stage he was at, his budget, his deposit, his income, whether there was anything we should know about his credit history. He worked through all of it and stopped one step short of picking a meeting slot. Nobody was woken. Nothing was rushed. By the time anyone at the firm looked, the entire exchange was sitting in the system, timestamped and ready to read back, because the conversation and the record of it were the same object. Timely support, provided and evidenced in a single motion.

It does not make you compliant. You do.

I keep hammering this because it is the line the whole piece turns on, and it is the line careless marketing crosses. No software ensures compliance with the Consumer Duty. The obligations fall on you, the regulated firm, and they always will. What good tooling does is narrow the gap between the good outcome you already deliver and the evidence the FCA now expects you to produce for it: a timely first response, a complete fact-find, a logged conversation, a client reached before the renewal window closed. It helps you evidence the outcome. It does not own it.

You do not have to take that from a vendor. The brokerage with the evening referrals had its compliance lead in that same meeting, and she spent it asking exactly the questions you would want asked: where the data lives, how it has been handled, why any rollout should start as a trial. On whether a regulated firm should be putting client conversations on WhatsApp at all, she was measured: the channel is accepted in financial services where it is used, in her words, "for good outcomes for the clients", though not yet recognised as the best way of approaching them. And then she put the responsibility precisely where it belongs.

"The regulators are not going to say it's not a good tool, but it's a business decision. If a business wants to use it, they're not going to stop you, but at the same time, you've still got the responsibility to make sure you're doing the right thing with the tool."

The person who looks after compliance at a mortgage brokerage

Notice the shape of that. She is not asking whether the tool is permitted. She is asking what her firm owes its clients while using it. The tool is a business decision. The responsibility does not move. That is the frame, from the person in the room whose job it is to say no, and it is the frame to hold every compliance-software conversation in, including this one.

Framed that way, the fear that automation depersonalises regulated advice mostly dissolves. The best brokers I work with do not see it as replacing the adviser. Someone I spoke to at a property group that runs its own mortgage arm said it better than I can.

"You're never going to remove the human interaction... It is not a replacement of... If you find that one in five of your mortgage clients are booked in because of this, great."

Speaking for a property group with an in-house mortgage arm

That is the right instinct, and it is the compliance-conscious one. Let the tool carry the reach and the record. Keep the adviser on the advice and the relationship.

The trail is automated. This is not. Suitability, the protection conversation, the judgement a couple is really paying for: the Duty puts all of it on the adviser, and no tool should want it anywhere else.

The turn, when it comes, is rarely a conversion. The adviser who told me about the heat going out of a lead had spent the first half of that same meeting saying he was nervous. His client relationships, he said, were personal and intimate, built over years, and he did not want to be turned into a volume operation. He was right to say it. But when someone on our side put it back to him that the only thing keeping a broker alive in the long run is exactly those relationships, his answer landed well short of enthusiasm.

"This probably aids that, but it's just something that we need to learn to embrace."

A mortgage adviser, on whether the tool threatens the client relationship

Not a conversion. A concession, hedged with a probably, from a man guarding the thing that makes him good at his job. I would take that over enthusiasm every time, because it is the sound of someone who has actually weighed it. The relief, when it arrives, is quiet, because the thing eating his evenings was never the advice. It was the admin around it.

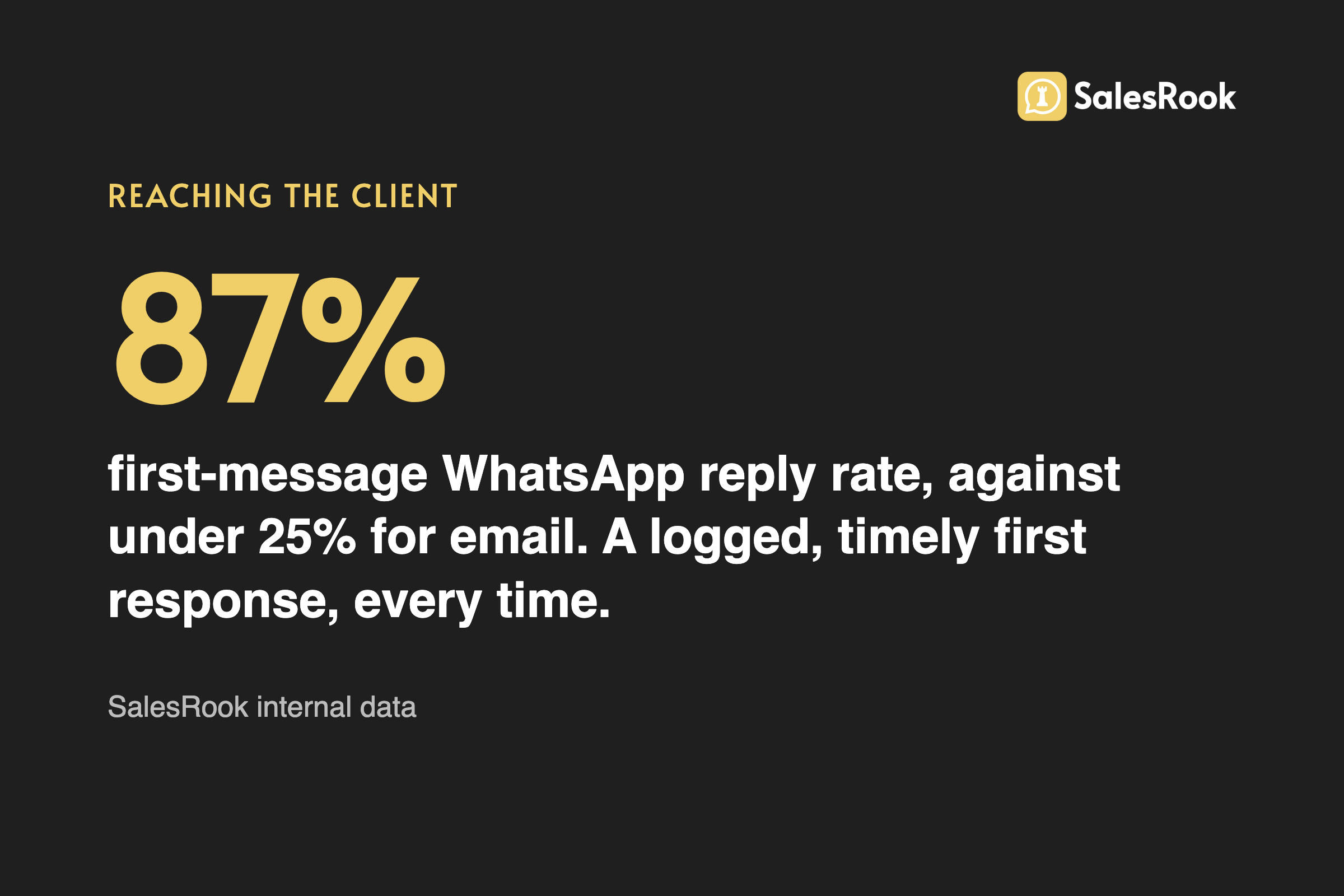

For what it is worth, on our own platform data, conversations opened this way see WhatsApp reply rates approaching 87%, against under a quarter for email. That is a SalesRook product figure, not an audited third-party result, and I will always label it as such. But a channel the client actually answers is not just a conversion story. It is the difference between a documented conversation and a voicemail nobody returned.

How to evidence good outcomes without drowning in admin

I would rather teach you to get this right, with any tool or none, than sell you a mystery. If the Consumer Duty is now an evidence problem, then whatever you use, hold it to this checklist. Most of it you can start tomorrow morning.

- Move client conversations onto a channel you own. No regulated advice on personal WhatsApp or a shared phone nobody can supervise. If you cannot log it, you cannot evidence it.

- Make the first response timely, and record when it happened. For the consumer-support outcome, the timestamp is a big part of the evidence. An out-of-hours or overflow safety net that captures the enquiry the moment it lands is worth more than a faster human you do not have.

- Take a complete, consistent fact-find every time. Consistency is a compliance asset. A process that captures the agreed questions the same way each time, with adviser review, is easier to stand behind than one that depends on how tired the adviser is.

- Reach renewals before the dead zone closes. Map your product-end dates and get to the client before the lender's default does. That is where the price-and-value evidence comes from.

- Keep the human on the advice. Automate the reach and the record, never the judgement. The Duty falls on the regulated firm, so the responsibility stays with the adviser, and so should the relationship.

- Produce the trail as a by-product, not a project. The goal is that your evidence is simply the logged conversation, not a separate file you assemble at reporting time.

The man who asked "where's the trail" was not being difficult. He was asking a practical version of the question the FCA now asks every regulated firm, and he already sensed his honest answer would not survive it. The good news is that the fix is not more effort or more forms. It is putting the conversation somewhere it records itself.

So here is the challenge. Better to set it for yourself now than have the regulator set it for you later. Pull your last ten renewal cases. For each one, ask a single question: could you show, today, exactly when you first responded and what was said? If the answer for even a couple of them is "it is on someone's phone" or "we called, I think", that is not a failing of your advice. It is a gap in your evidence, and it is entirely fixable.

If you would like to see what that looks like on your own enquiries, in your firm's voice, with the evidence captured as it happens, we build exactly this for mortgage brokers. Take a look at how it works, or give us a week of your enquiries and we will show you the trail it leaves behind. Then you can answer those opening questions without checking anyone's phone.

Max Hardy

Co-Founder

Max Hardy is the Co-Founder of SalesRook, a leading provider of AI solutions for the property sector. With a background in technology and property, Max leads SalesRook's mission to transform how estate agents and mortgage brokers engage with leads through AI-powered WhatsApp automation.